By the end of 2022, Asia had installed nearly 5.9 GW of floating solar capacity — up from 210 MW in 2016. In the same window, the average size of a single FPV project went from a few hundred kilowatts to several hundred megawatts. China, India, Taiwan, Japan, Korea and Indonesia have between them deployed hundreds of systems and built a complete industrial ecosystem — module suppliers, mooring specialists, EPC contractors, financiers — around a technology that barely existed at scale a decade ago.

Africa, with stronger physical conditions for FPV than most of Asia, has installed less than 25 MW. The gap is not a technology problem. It is an execution and capital problem, and the Asian experience tells us how to close it.

What actually happened in Asia

Before drawing lessons, the trajectory is worth understanding. Asian FPV did not grow steadily. It accelerated in step changes triggered by policy decisions, infrastructure adjacencies, and a small number of demonstration projects that proved the case to capital and regulators.

China provided the early scale. Coal-mining subsidence ponds in Anhui and Shandong provinces — disused water surfaces with adjacent grid infrastructure — became the proving ground for projects of 40 MW, 70 MW, and eventually 150 MW. By 2018, China alone had installed more than 1 GW of FPV. The country had no specific FPV policy. What it had was utility-scale solar tariff support, abandoned mining infrastructure adjacent to load centres, and developers willing to put steel on water.

Japan and Taiwan ran a different playbook — high-density, smaller projects on irrigation ponds and aquaculture lagoons under feed-in tariff regimes. Korea built large reservoir-based projects backed by state utility KEPCO. India moved later but moved hard, with reservoir-based FPV designated as a strategic deployment vector and projects such as Ramagundam (100 MW) operating, and Omkareshwar (600 MW under development) anchoring a national pipeline.

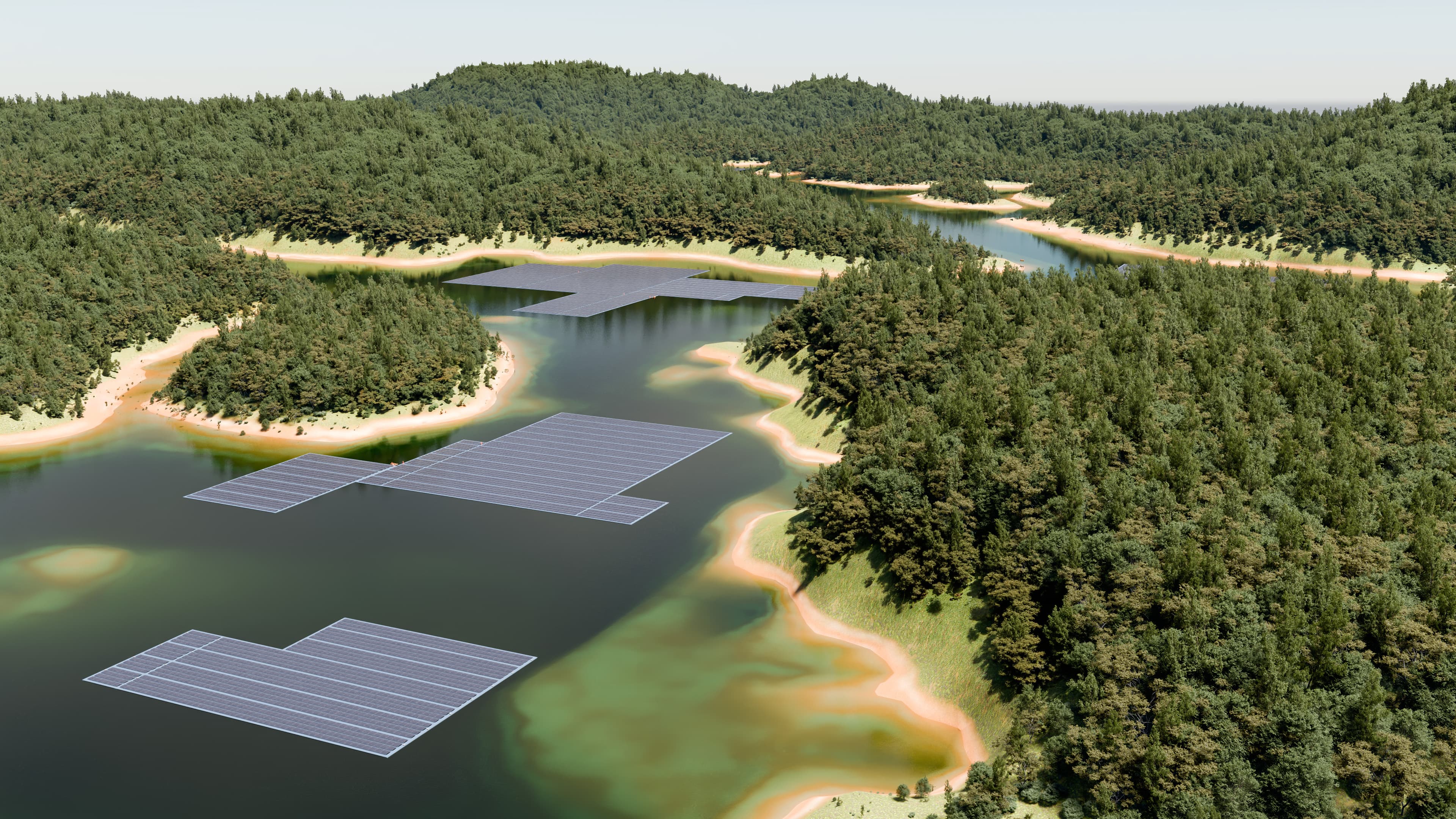

The most directly relevant project for African developers is Cirata in Indonesia. Commissioned in 2023 on an existing 1,008 MW hydropower reservoir, Cirata is currently 145 MWp, with expansion to several hundred MW planned. It is a hybrid hydro-FPV asset, jointly developed by Masdar and Indonesia's state utility PLN, financed by a consortium of international banks. It is, in effect, the template for what large-scale FPV on a tropical hydropower reservoir looks like.

The lessons that travel

Several patterns hold across these markets, and all of them are directly relevant to Africa.

Anchor on existing infrastructure. Every successful Asian FPV market started by deploying on water bodies that already had grid connection, dam access, and operational management — coal subsidence ponds, hydro reservoirs, irrigation lakes adjacent to substations. The capex burden of new transmission and access infrastructure is what kills early-stage projects. By starting on existing assets, Asian developers avoided the most expensive enabling work and proved bankability before tackling greenfield.

For Africa, this points first at hydropower reservoirs. The continent has 42 GW of operating hydro, almost all of it with substations, transmission corridors, and access roads already in place. The Tchimbélé reservoir in Gabon, where our first project sits alongside a 69 MW operating hydro station and feeds into transmission lines that already export power to Libreville, is exactly this archetype.

It also points at coastal lagoons, which are the most underexploited large water bodies on the continent. Lac Togo in Lomé, the Ébrié lagoon in Abidjan, sections of the Beninese and Nigerian coast — each represents tens of square kilometres of calm, low-wave water surface within a few kilometres of metropolitan demand and existing transmission. Lake Togo, where Green Energy Ventures is in early-stage development for a 50 to 100 MWp project, sits adjacent to the West African Power Pool corridor and within the immediate catchment of Lomé's load. Lagoons are land-neutral, generally close to urban load centres, and free from the agricultural land-use conflict that constrains ground-mounted solar. For coastal African markets, they are the second natural anchor point after hydro reservoirs — and in some geographies, the more strategically positioned of the two.

Sovereign offtake matters for the first projects. Cirata sells to PLN. Ramagundam sells to NTPC. Korean projects sell to KEPCO. The Asian FPV market did not start with merchant tail-risk financing — it started with creditworthy state offtakers under long-term PPAs. That structure de-risked the technology for lenders and allowed the cost of capital to compress as track record built.

The implication for Africa is not that every project needs a sovereign guarantee. It is that the first generation of utility-scale projects on the continent should be structured around state utility offtake, ideally with a sovereign-backed PPA, while the technology earns its bankability spurs. Merchant or PPA-light structures can come later — once 200 to 300 MW has been delivered and operating data exists.

Project sizes scaled faster than anyone predicted. The leap from 1 MW pilots to 100+ MW utility-scale assets took five to seven years in most Asian markets, not the fifteen to twenty years that solar took on land. The reason is that FPV is not a new technology in any meaningful sense — it is photovoltaic modules on engineered floats. Once the first project at scale is delivered, subsequent projects do not face technology risk; they face execution risk, which is solvable.

For African developers, this means the right ambition is not a 10 MW pilot followed by gradual scaling. It is a first project at 50 MW, followed by 100+ MW projects in the next 24 to 36 months. The market will reward whoever moves at scale first, because development costs are largely fixed and the bankability premium accrues to the first mover.

A local supply chain follows scale, not vice versa. Asian FPV component suppliers — Ciel & Terre's Asian operations, Sungrow Floating, Korean and Chinese mooring specialists — emerged because there was deployment volume to justify localisation. Africa does not yet have this. The first 500 MW will be delivered with imported components and international technical partners. The next 5 GW, if it materialises, will support a continental supply chain. This is the natural sequencing, and it is wasted effort to try to build the supply chain before the demand exists.

Hybridisation is the financial multiplier. Cirata is a hybrid project. Many of the larger Korean and Chinese projects co-locate with hydro or thermal assets. The reason is that hybridisation does two things at once: it improves system economics (water savings, firming, grid services) and it lowers the cost of capital — an existing utility-scale asset with established cash flows is a stronger collateral base than a greenfield site. African developers who position FPV as a hybrid layer on existing hydro, rather than as a standalone technology, will find capital more available.

What is different about Africa

The lessons travel, but not perfectly. Two differences matter.

First, the policy environment is more fragmented. Asia benefited from large national markets — China, India, Korea, Japan — where a single regulatory regime supported scale. Africa is 54 countries. The implication is that the first-mover developer needs a multi-country pipeline rather than a single-market platform; market risk in any one jurisdiction is too concentrated. This is why our portfolio thesis — 500 MW across multiple geographies — is structured the way it is.

Second, capital cost is higher. Asian FPV grew up alongside cheap state-directed bank lending. African projects will need to blend commercial debt, DFI guarantees, and equity in ways that Asian projects did not. The structuring complexity is real, but it is solvable — and it is not, in itself, a reason for the technology to fail to scale on the continent.

The honest assessment is that Africa is roughly where Asian FPV was around 2015 to 2016 — proven technology, isolated demonstration projects, no utility-scale precedent, but strong physical and economic conditions. Asia closed that gap in five years. Africa has the data, the infrastructure, and the demand to do the same.

Sources

- SERIS Global FPV database (2022)

- Masdar / PT PLN public disclosures on Cirata (2023)

- NTPC public disclosures on Ramagundam

- Indian Ministry of New and Renewable Energy on Omkareshwar

- Global Atlas of Marine Floating Solar PV Potential